FY25 Review: Markets Close FY25 with Strength Despite Policy and Geopolitical Headwind

Structuring, building, and managing your portfolio with complete transparency and accountability — aligned to your goals and values.

Dear Investors,

Australian and global equity markets wrapped up the 2025 financial year on a strong note, staging an impressive recovery from April’s sharp correction. Despite heightened volatility driven by international trade tensions, elevated tariffs, and escalating geopolitical concerns, risk assets bounced back, with the ASX and global indices posting solid full-year gains.

The volatility began early in the June quarter, when President Trump announced sweeping tariffs on most U.S. trading partners, sparking fears of a global slowdown. Markets reacted sharply, with global indices including the S&P 500 initially falling ~20% and dragging local sentiment with them. However, a series of de-escalatory measures—including reduced tariff rates, exemptions on key imports such as semiconductors and pharmaceuticals, and favourable court rulings—restored confidence. These developments, alongside robust economic data and strong corporate earnings, fuelled a recovery into June and allowed markets to end FY25 at or near all-time highs.

The rebound accelerated through May and June, aided by a significant reduction in Chinese tariffs, ongoing strength in the tech sector (notably AI-linked stocks such as Nvidia and Oracle), and renewed optimism that economic growth could withstand the tariff environment. Even a spike in oil prices following Middle East tensions failed to derail markets for long, with energy prices retreating and equity markets rallying into the final days of the financial year.

4Q Performance Review

The fourth quarter started with a proverbial thud as, on April 2nd, President Trump announced sweeping and substantial tariffs on virtually all U.S. trading partners. The tariff amounts were significantly larger than markets expected and their announcement sparked fears of a trade-war-driven economic slowdown, which hit stocks hard as the S&P 500 entered correction mode, down over 20% from the highs. However, that low in the index on April 8th turned out to be the low for the quarter as the rest of April saw the administration take numerous steps to reduce the practical impact of those announced tariffs.

A week after reciprocal tariffs were announced, the administration declared a 90-day delay where tariff rates on most trading partners would be just 10%, far below most reciprocal tariff rates. That delay was then followed by more steps to reduce the tariff burden, including important exemptions for key imports such as smartphones, semiconductors, pharmaceuticals and computers. The delay in reciprocal tariff rates and key category exemptions gave investors some confidence that the trade war would not automatically cause a recession, and that optimism combined with a solid quarterly earnings in the US helped the S&P 500 rally throughout the remainder of April and close with just a slight loss, down 0.68%.

The market rebound accelerated in May as Treasury Secretary Scott Bessent announced he would be meeting with Chinese trade officials in Geneva early in the month. That boosted investor expectations for more tariff relief and those hopes were fulfilled as the meeting resulted in a dramatic reduction in tariffs on Chinese imports from 145% to approximately 30%. That tariff reduction combined with still-solid economic growth further eroded investor concerns that tariffs would cause a recession and stocks extended their rebound, in Australia and abroad.

Earnings also contributed to the rally thanks to strong results from tech bellwether Nvidia (NVDA), which reminded investors of the growth potential of artificial intelligence (AI). Finally, in late May, the Court of International Trade ruled the administration’s tariffs were illegal under the law used to justify the duties.

The case was appealed immediately and a decision should come in 1Q25, but the initial ruling raised the prospect that tariffs could be eliminated almost entirely by the courts in the coming months. That decision further strengthened the belief that tariffs would not derail the strong economy, and stocks turned positive year to date and finished May with very strong gains, up more than 4%.

The rally continued in June although trade headlines, which had driven market moves for the first two months of the quarter, took a back seat to geopolitical concerns after Israel launched a massive attack on Iranian nuclear and military facilities. The hostilities between the two rivals caused oil prices to temporarily spike and that halted the rally in mid-to-late June, as investors again had to consider the prospect of rising oil prices hurting economic growth and boosting inflation.

However, that volatility was limited, as following U.S. strikes on Iranian nuclear facilities, a ceasefire was agreed to between Iran and Israel and oil prices dropped sharply, turning negative for the quarter. That decline, combined with rising expectations for rate cuts in the second half of the year, pushed stocks towards or above new all-time highs.

To sum up, volatility during the quarter was extreme, but the stock market ultimately completed an impressive rebound from the steep declines of early April, as steps by the administration to ease the tariff burden helped to boost investor confidence while corporate earnings remained strong and economic growth proved resilient, yet again, even in the face of geopolitical uncertainty and elevated policy volatility.

Under the hood

Despite a volatile final quarter, Australian and global markets ended the 2025 financial year with strong momentum. Local shares followed global counterparts higher in June, as fears around tariffs, inflation and geopolitical risks subsided, and investor optimism returned. The ASX 200 delivered a positive full-year return, supported by strength in large caps and rate-sensitive sectors, even as headwinds persisted in energy and smaller companies.

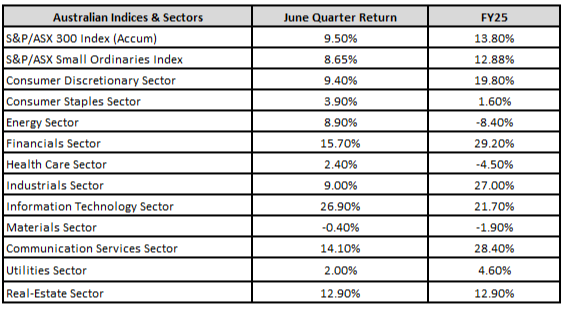

Australian Equities – Positive Finish to FY25

The Australian share market, like much of the developed world, saw a sharp selloff in April, initially triggered by tariff announcements out of the U.S. and broader concerns over global growth. However, as policy fears eased, and economic data remained firm, confidence returned. The rally into June helped the ASX 200 lock in a solid full-year result.

Large caps outperformed small caps through FY25, with the major banks, telco’s and retailers’ proving resilient in the face of macro uncertainty. Tech also had a standout year, benefiting from the global AI tailwinds and reduced pressure from rising interest rates.

Growth stocks led the way, mirroring trends seen globally, as sectors tied to innovation and structural tailwinds (such as AI and digital infrastructure) attracted fresh capital. Value and cyclical sectors, including energy, materials and traditional industrials, struggled to keep up, particularly amid volatile commodity pricing.

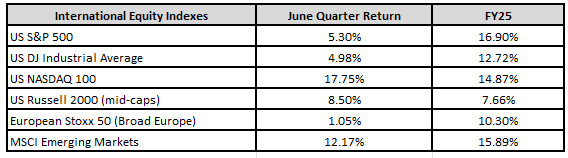

Global Equities – A Tailwind for Diversified Portfolios

International equities were a strong contributor for Australian investors in FY25. U.S. markets, particularly the tech-heavy NASDAQ 100, rallied sharply in the final quarter thanks to tariff reductions, strong corporate earnings, and optimism around rate cuts later this year. Emerging markets also rebounded, buoyed by improving data from China and cooling tensions in the trade relationship with the U.S.

A falling US dollar detracted from AUD domiciled returns during the year.

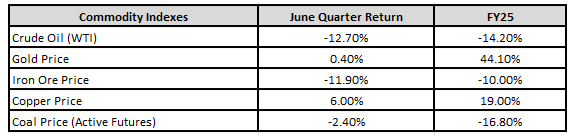

Commodities – Gold Glitters, Energy Wavers

Commodities presented a mixed picture. Gold surged over FY25, supported by safe-haven flows and a weaker USD, benefiting Australian producers and ETF investors. Oil, by contrast, weakened late in the year despite geopolitical flare-ups in the Middle East, as demand forecasts softened and risk premiums faded. Iron Ore had another softer period, as did Coal, while Copper remained well supported. The net result was a drag on iron ore & energy sector earnings and share prices, particularly in April and May.

Fixed Income – Bonds Regain Footing

Bonds enjoyed a more constructive period into year-end, with falling inflation prints and hints of monetary easing ahead supporting demand for duration. Australian fixed income returns improved steadily across the second half, with long-dated government and high-quality corporate bonds outperforming cash and short-term instruments.

Investors began to anticipate potential RBA cuts in late 2025 or early 2026, amid signs that the post-COVID rate hiking cycle had peaked. High-yield bonds also fared well, reflecting renewed investor confidence in corporate balance sheets and a better-than-expected growth backdrop.

FY26 Market Outlook

The markets begin FY26 at or near all-time highs, following an impressive FY25 performance despite much-larger-than-expected tariffs on U.S. imports, a dramatic increase in policy volatility and more hostilities in the Middle East.

While investors expected tariffs and a tougher stance on trade from the new administration, the moves taken exceeded the vast majority of expectations as tariffs were both higher and more far reaching than most expected.

Tariffs matter to the markets primarily because, if not properly executed, they could cause an economic slowdown, or worse, stagflation, where growth slows but inflation rises. Fears of a tariff-induced slowdown or return of stagflation were contributing factors behind the April decline in stocks.

Positively, economic data remained mostly resilient throughout the period and there are no major economic indicators pointing to a material slowing of growth or a sudden rise in inflation. That resilient data in the face of tariffs and geopolitical turmoil contributed to the market rebound.

Finally, geopolitical risks undoubtedly rose with direct conflict between Israel and Iran (including U.S. involvement in the war) and no progress on a ceasefire on the now three-year-long war between Russia and Ukraine. However, the market views these conflicts as largely isolated and not at risk of spreading into a larger regional war that could disrupt oil production or the global economy. Because of that, markets largely ignored the increase in geopolitical tensions.

However, while the market was impressively resilient over the past three months, it would be a mistake for investors to become complacent in this environment, because there remain a lot of risks facing the economy and markets.

First, while the market has assumed that tariffs won’t rise substantially from current rates, there’s no guarantee of that. To that point, the deadline for the reciprocal tariff delay is July 9th and if that deadline is not extended, we could see tariff rates on major trading partners surge once again. Regardless, the reality is that global tariff rates are at multi-decade highs and it’s still uncertain how that will impact the economy in the months ahead (so risks of a tariff-induced slowdown or rise of stagflation can’t be dismissed).

Turning to geopolitics, while the various conflicts have not negatively impacted global markets, risks remain elevated. If Iran takes steps to disrupt global oil production or transit, that will boost oil prices and create a new headwind on markets. Similarly, if these isolated conflicts begin to spread into larger regional conflicts that will also lift oil prices and weigh on stocks and bonds.

Finally, investors expect two interest rate cuts in the US, and at least three in Australia between now and year-end; however, the unknown impact from tariffs on economic growth and inflation make rate cuts in 2025 far from certain. If central banks do not cut rates in the coming months, that will increase concerns about an eventual economic slowdown and that could weigh on markets.

Bottom line, markets have been impressively resilient so far this year, but as we start FY26 there remain numerous, potentially significant risks and we will not let the market’s resilience create a sense of complacency.

To that point, at Market Partners, we remain committed to helping you effectively navigate this investment environment.